If you’re self-employed, getting a home loan can be trickier. Lenders want to see consistent income, and if yours fluctuates or you minimise tax, it can raise red flags.

According to the Australian Small Business and Family Enterprise Ombudsman, there were 1.7 million self-employed Australians in June 2024. This was 4.9% more than in 2023 and made up 62.5% of all businesses in the country.

Despite this growing segment, many self-employed Australians face additional hurdles when applying for a home loan. But here’s the good news: with the right preparation and expert help, self employed home loans are well within reach.

Why self-employed borrowers face more challenges in getting a mortgage

Lenders can sometimes see self-employed applicants as a higher risk. That’s because:

-

Your income can fluctuate, making it harder to assess borrowing power.

-

Tax deductions can reduce your taxable income on paper, which may make you look less financially capable, even if your cash flow is strong.

-

Your income is more difficult to verify as you don’t have traditional payslips like a salaried employee. You need to rely on tax returns and financial statements, which may not always reflect the true picture.

In addition, the application process can be more involved. You’ll typically need to provide full tax returns, business financials and other supporting documents.

Many lenders also require that your business has been operating for at least two years and ideally with a consistent or upward income trend. Without this track record, your chances of approval may be reduced.

Key documents required for a self-employed home loan application

If you’re applying for a self employed home mortgage, expect to provide detailed records. That’s because lenders want to see both how much and how consistently you earn.

Here’s what you’ll typically need:

-

Personal and business tax returns for the last 1–2 financial years

-

Business financials including a profit and loss statement and balance sheet

-

Business Activity Statements (BAS) or bank statements to verify ongoing income and expenses

-

ABN and GST registration details (especially if you’re a sole trader or contractor)

Some lenders may request interim financials if you’re applying mid-financial year, or if your most recent tax return doesn’t reflect your current income.

Clean, accurate and up-to-date financials can make all the difference. It’s worth working with your accountant early to ensure your numbers tell the right story.

Full-doc vs low-doc loans: which one should you choose?

When applying for self employed home loans, you’ll generally have two main options: full-doc or low-doc. Which one you choose depends on how much financial documentation you can provide and how strong your numbers are.

Full-doc loans

These are the most common options for self-employed borrowers who can provide at least two years of consistent, verified financial information.

Full-doc loans often offer access to a broader selection of lenders, potentially resulting in more competitive interest rates and additional features like offset accounts and redraw facilities.

Low-doc loans

Low-Doc loans are designed for self-employed borrowers who can’t meet the standard documentation requirements, such as those who have recently started their business, haven’t completed recent tax returns or have income that’s difficult to verify in traditional ways.

Instead of relying on full tax returns and profit-and-loss statements, low-doc lenders may accept alternative forms of income verification. These can include recent business bank statements, BAS statements or a signed letter from your accountant confirming your income.

While low-doc loans provide more flexibility, they can also come with trade-offs, such as higher interest rates and larger deposit requirements.

Strategies to improve your mortgage approval chances

Even though mortgages for self employed borrowers require more legwork, there are smart ways to boost your approval chances, especially if you start preparing early.

Here’s how to get your finances in shape:

-

Keep taxable income high: Avoid excessive deductions in the one to two years before applying.

-

Reduce your debts: Paying down credit cards, personal loans or business liabilities can improve your debt-to-income ratio.

-

Save for a bigger deposit: Aim for at least 20%. A larger deposit shows lenders you’re financially responsible and have more skin in the game. This reduces their risk and can improve your chances of approval. As a bonus, it can also help you avoid paying lenders’ mortgage insurance (LMI).

-

Improve your credit score: Improving your credit score shows lenders that you can manage debt effectively. Pay off overdue accounts, avoid multiple credit applications and keep business and personal debts separate.

The key is to plan ahead. Aim to start preparing at least 6–12 months before you apply. This gives you time to get your finances in shape, improve your credit position and build a strong case for your loan application.

Alternative lenders & non-traditional mortgage solutions

When it comes to self-employed home loans, not all lenders operate the same way. Traditional banks tend to have strict rules, especially around income verification and business history, which can make approvals difficult.

That’s where alternative lending options come in.

First, non-bank lenders are regulated financial institutions that aren’t banks. They often assess applications more flexibly, which can help if you have a newer business, irregular income or a complex structure. Many accept alternative income verification, like BAS or bank statements.

Non-bank lenders offer traditional loan products (like home loans, asset finance or vehicle loans), but often with more flexible criteria than major banks. Their turnaround times can be quick, with fast assessment criteria.

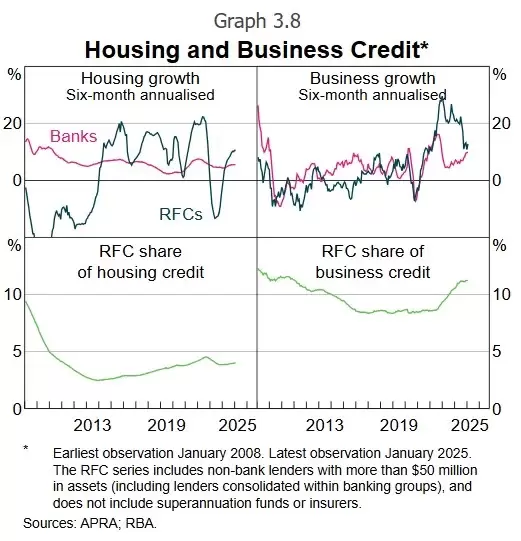

According to the Reserve Bank of Australia, non-bank lending is growing rapidly. In 2024, it accounted for 6% of financial system assets.

As the graph below shows, RFCs (or registered financial corporations, which make up around half of non-bank lenders by size) grew their share of housing lending over 2024 at a faster rate than banks.

Private lending is another alternative source of self employed home loans. These lenders, often individuals or small groups, may offer short term or bridging loans, especially useful if you’re waiting for updated financials or tax returns.

So, when should you consider alternative financing over a traditional bank?

Well, if you’re struggling to meet tough serviceability requirements or can’t supply two years of tax returns, alternative lenders may offer a more flexible path. Many accept alternative income verification, such as BAS statements or accountant letters.

Just keep in mind, interest rates can be higher and some features may be limited. A mortgage broker can help weigh the trade offs and find the right option for your situation.

Also, don’t overlook government schemes. Depending on where you’re buying and your circumstances, you may still qualify for First Home Owner Grants, stamp duty concessions or other support, even if you’re self-employed.

Why working with a mortgage broker makes a difference

Applying for a self employed home mortgage either you are a doctor or lawyer takes careful planning, tailored strategy and, in some cases, a bit of negotiation. That’s where a mortgage broker can make a big difference.

Mortgage brokers:

-

Have access to lenders who specialise in self-employed clients

-

Know what documents to prepare

-

Understand lender policies

-

Can negotiate favourable rates and terms

Applying directly with a bank is an option, but if your application is rejected, it can impact your credit file and reduce your future borrowing options. This is especially risky for self-employed borrowers.

A broker helps you avoid these pitfalls by matching you with the right lender from the start.

Plus, brokers are bound by best interest duty. We’re required to recommend the loan that’s right for you, not one that pays us the most.

Final steps to a successful mortgage application

Want to give yourself a good chance of approval? Here’s a final checklist:

-

Start early: Ideally, 6 to 12 months before you plan to buy

-

Get your books in order: Ask your accountant to prepare lender-ready financials

-

Keep your income consistent: Avoid big business changes or cash flow spikes

-

Work with a broker: We’ll help flag any red flags before your application reaches the lender

By planning early and getting expert guidance, you’ll avoid delays and boost your chance of approval.

How we help self-employed buyers get approved

At AXTON Finance, we specialise in helping self-employed Australians secure the self employed home mortgage that suits your financial citation and long-term goals. Whether you’re a sole trader, freelancer, company director or contractor, we understand the ins and outs of mortgages for self employed clients.

Our team will take the time to understand your business, help you gather the right documentation and match you with lenders that make sense for your situation. We’ll do the hard work, so you can focus on growing your business and planning your next move.

Self-employed and ready to buy a home? AXTON Finance can help business owners secure the right loan with the right lender. Call 03 9939 7576, email getabetterrate@axtonfinance.com.au or get in touch to get started.